As a property investor or first-home buyer we often get preoccupied with when is the best time to buy often delaying the purchase to pick the perfect time. What everyone is trying to avoid is buying a property and then watching it drop in value and wishing they had just waited for a better deal.

Many investors believe time in the market is more important than timing the market and we agree. So when is the best time to buy an investment property? The obvious answer is the bottom or the trough but there are number of factors to consider such as identifying when that actually is and whether you are ready to buy at that time. As the market nears the bottom of the trough look for vacancy rates beginning to tighten as excess supply in the market is taken up during the counter cycle. This will eventually force rents to increase as the vacancy rate gets below the 3.0% equilibrium mark. Once rents increase, price increases eventually follow. Most people buy at the top half of the cycle as this is when they feel most safe and credit is freely available.

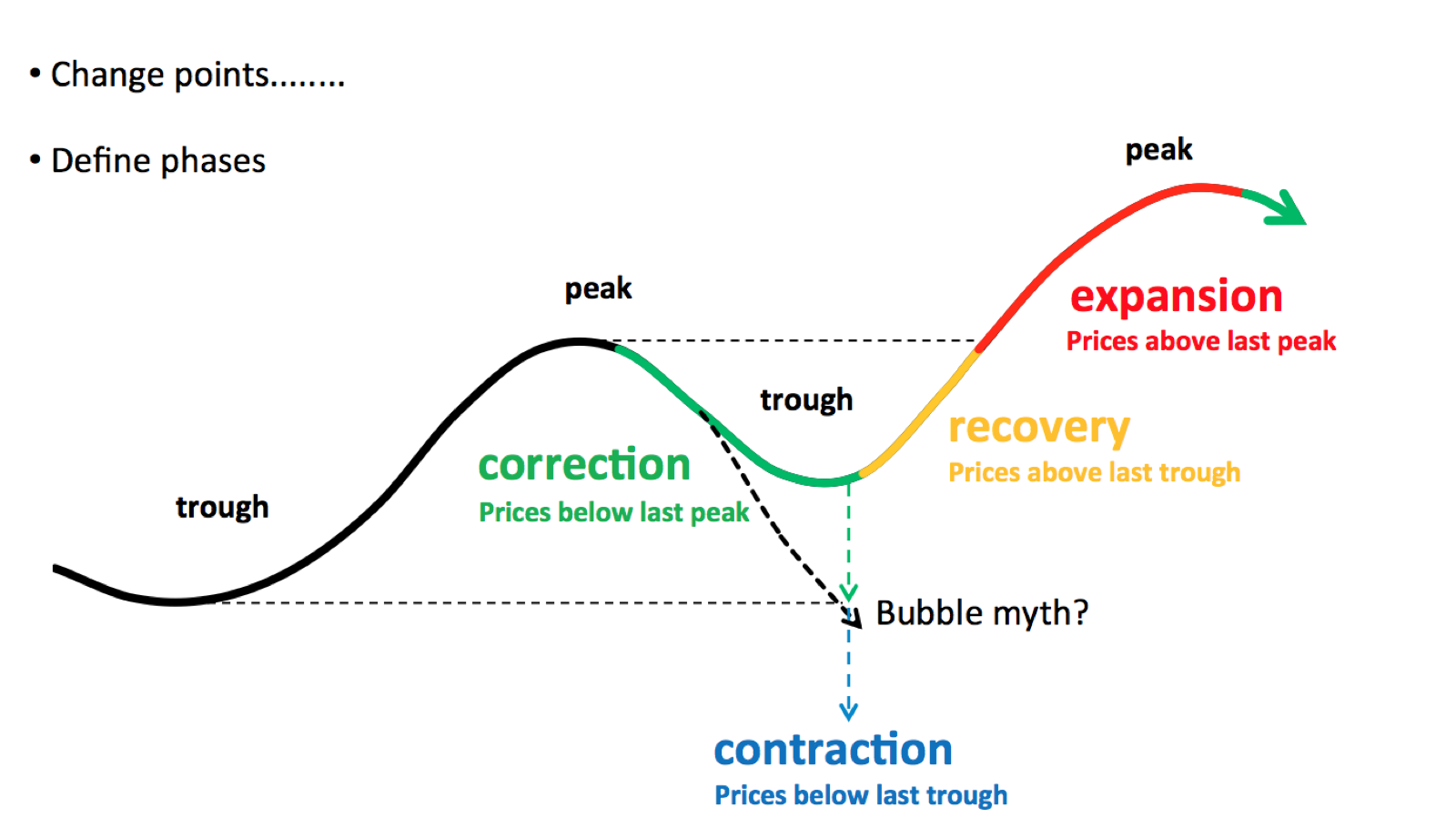

The Wilson curve depicted by Dr Andrew Wilson shows the property cycle typically seen in capital city locations with the current trough higher than the previous one indicating an upwards movement of prices over time despite slowdowns in the market. The time between peak cycles is usually 7-10 years.

The Sydney market is going through a downward cycle at the moment with prices peaking in July last year after it reached a height of 75% above its previous peak. Capital city downward cycles typically last 12-18 months so Sydney could be only 6-12 months away from the bottom of the next cycle. So far median prices have only dropped 3.1%. Buying in the downward cycle also know as the counter cycle can also be a great time to buy with the ability to negotiate a great deal with vendors who are also uncertain about where the bottom of the cycle is. To do this however requires courage and to get courage requires experience. It always helps if you have been through a property cycle or two and have some perspective on what is happening while others are panicking.

The Perth market last reached a peak in mid 2014 so has been on a downward cycle for the past 36 months. Median prices are about 10% below their previous cycle peak. Vacancy rates are beginning to tighten now indicating there will soon be pressure on rents. Further evidence of a bottoming market is the quarter to to 30 Nov 2017 showing positive growth in the Perth market for the first time since late 2014 with a 0.3% increase Unfortunately the most recent quarter to 31 Jan 2018 (Nov/Dec/Jan) showed a (0.3)% decline largely reversing those gains.

Melbourne peaked at 59% above its previous peak in November last year and has shown a very modest fall in prices in the past 2 months of (0.4)% showing that it a more resilient property market than Sydney with better affordability, higher population growth and a stronger performing local economy.

Brisbane last had a peak prior to the GFC in late 2010 and has been on an upwards swing since 2013 enjoying 5 years of modest price growth now about 16% above its previous peak. The rate of growth has been slowing within the past 12 months to Jan 31 2018 being 2.1% and the past quarter flat at 0.1%. Perhaps this market is reaching its peak again with all of the South East Queensland growth going to the Gold Coast and the Sunshine Coast with these areas growing at least twice as fast as Brisbane in the past 12 months.

So when is the best time to buy? Buying at different stages in the property cycle all have their advantages and disadvantages so anyone could argue that timing the market is most important and each of these arguments all have their merits. Knowing when that time is can be hard to know especially if you are a first-time property investor or first-home buyer.

What is most important is to make sure you purchase when you can comfortably afford to do so. The worst thing that could happen is that you are forced to sell your property and you lose some or all of your hard saved deposit. If you purchase close to a capital city and you borrow within your means then you could withstand a short period of decline. As a first-home buyer it really does not matter if the median price declines for a short period of time unless you are forced to sell. The only reason you would be forced to sell is if you borrowed too much and did not allow for a 2-3% interest rate increase over the cycle. This equates to $2,000 to $3,000 per annum on every $100,000 borrowed or roughly $50-60 per week. If you are a property investor then you need to allow for the possibility of lower rents during the downward cycle. Better to accept a period of lower rents than hanging out for a higher rent with extended vacancy. Lower rents means you property may go from cashflow positive to negative for a short period of time. Once again allow for a cash buffer to cover this. The good thing about buying near a capital city is that the timing of the next cycle is never too far away.

It is more important to get into the market than delay and miss out on an opportunity to build equity over time.