I have heard a lot of strange reasons why someone does not want to buy a property that is perfectly suited to their strategy. Often these opinions have been formed through their own research online, reading the news or conversations with friends and family.

We have listed our top 5 here and explain why they are just myths.

1. There is too much land supply available in a masterplanned community for prices to go up

Masterplanned communities present one of the best ways to make capital growth with a house and land package however a lot of property investors pass up on this opportunity due to a concern that there is just too much land to be released in the future to allow any capital growth.

For property to go up in value over time demand has to outstrip supply right? This is exactly what happens in a masterplanned community due to limited planned stage releases and high owner occupier ratios that create a frenzy of buying activity - the land is both affordable and limited in supply leading to demand outstripping supply in some cases 10 to 1 . What you also get is an effective discount in the early stages due to strict land developer covenants, a strong pipeline of infrastructure, retail & commercial facilities, schools, hospitals, community facilities and transport upgrades both within and nearby the estate that make the land value go up over time.

Masterplanned communities can take 10-20 years to be fully developed with hundreds of stage releases but you are almost guaranteed capital growth. Masterplanned communities are just like a mini local government area. All land is not sold and built at once, it takes time for a community to take shape and flourish. One thing we look out for are the amount of double storey homes in the estate. This is an indication that there are a lot of owner occupiers living in the estate and they are willing to spend more money in the area. This is great for valuations and adds huge value to the land that is yet to be released.

2. New properties are always overpriced so you are better off buying an existing property

This is a common argument for people who want to spend as little as possible. There is a reason why a $430,000 four- bedroom house that is 10 years old is $70,000 less than a brand new house and land package in the same estate. It is not a $70,000 saving. You get no depreciation on fixtures and fittings and limited depreciation on the building. Tenants will pay lower rent and it is more likely to be vacant than a new property. Your builder warranty has also expired and any damage whatsoever is as your cost.

If your budget is $430,000 buy a new property for that price not a second hand one.

3. I want the most cashflow I can get and am not interested in capital growth

So if you bought a property today and it was worth the same in 20 years you would be OK with that? Oh Ah no but...

What are you really trying to achieve here. Replace your income with property so you can quit your job as soon as possible?

Here are the realities of this strategy. Lets say you have an income of $100,000 and want to replace it with property income. You would need almost 16 properties earning you $6,000+ per annum cashflow. These properties would cost you approximately $500,000 each meaning you would need $800,000 (10% deposit minimum) in equity plus another $400,000 in acquisition costs (5%). So unless you have $1.2m in cash or surplus available equity then this could take you decades to achieve this.

With capital growth on the other hand you can create wealth of $25,000 per annum and growing on a $500,000 property with just a 5% growth rate. A lot higher than the $6,000 cashflow which you would have to pay tax on anyway reducing your return again.

Why would you accept $6,000 per annum and a tax bill when you can get $25,000 per annum and no tax bill for each property you own? The only reason you may choose this strategy is you need the additional cashflow to increase your serviceability on your loan or you are nearing retirement and want to focus on income.

4. Property prices double every 10 years

This has been possible in the past but is not always going to be the case. That is a tad over 7% growth per annum for ten years in a row or 7.2% to be exact.

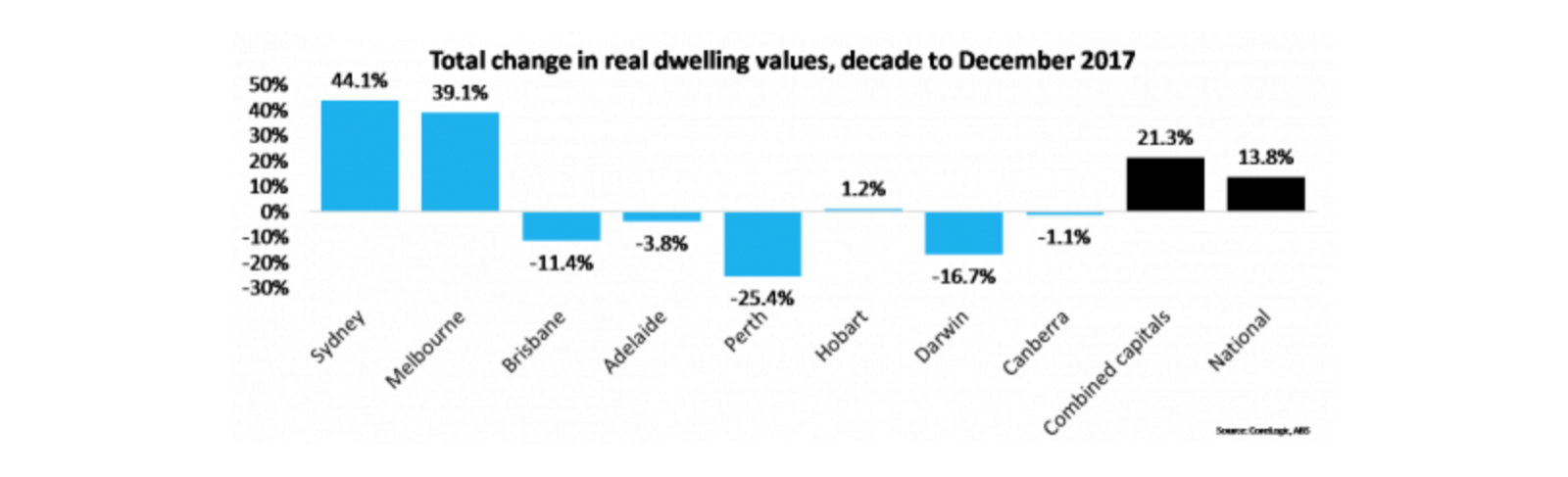

You also need to take inflation into account to calculate the real return. Remember inflation decreases the purchasing power of money over time as your costs go up. CoreLogic just released a report in Feb 2018 which showed that real dwelling values had only increased in 5 of the 8 capital cities and nowhere near doubling.

You need to assume a lower rate of return and be comfortable with this. A more realistic return would be property prices doubling every 15 years or just under 5% return.

5. Buying sit and forget capital growth properties is the slow way to create wealth

Yes it can be boring that is why we need to save you from yourself here. Unless you have a lot of experience and have a number of properties that are giving you capital growth then you need to lay the foundations for your financial future before you can go and do something more 'exciting' like a renovation or a small development so that if the project doesn't turn out like you expected you still have another property building you wealth over the medium to long term.

With moderate compounding returns a $500,000 property bought today can provide long term average wealth creation of well over $100,000 per year or more. This may be considered boring by some but is important if you are serious about wealth creation. Trying to achieve this by renovating and flipping properties or undertaking a small development each year is very difficult after allowing for taxes and agent's selling costs. Even the best in the game have problems doing this consistently.